Read? Wise Words Series - Part 2

"We become what we behold. We shape our tools and then our tools shape us." Larry Williams

Rule 1. It's all about survival

No platitudes here, speculating is very dangerous business. It is not about winning or losing, it is about surviving the lows and the highs. If you don't survive, you can't win.

The first requirement of survival is that you must have a premise to speculate upon. Rumors, tips, full moons and feelings are not a premise. A premise suggests there is an underlying truth to what you are taking action upon. A short-term trader's premise may be different from a long-term player's but they both need to have proven logic and tools. Most investors and traders spend more time figuring out which laptop to buy than they do before plunking down tens of thousands of dollars on a snap decision, or one based upon totally fallacious reasoning.

There is some rhyme and reason to how, why and when markets move - not enough - but it is there. The problem is that there are more techniques that don't work, than there are techniques that do. I suggest you spend an immense and inordinate amount of time and effort learning these critical elements before entering the foray of financial frolics.

9. Your fortune will come from your focus - focus on one market or one technique.

A jack of all trades will never become a winning trader. Why? Because a trader must zero in on the markets, paying attention to the details of trading without allowing his emotions to intervene.

A moment of distraction is costly in this business. Lack of attention may mean you don't take the trade you should, or neglect a trade that leads to great cost.

Focus, to me, means not only focusing on the task at hand but also narrowing your scope of trading to either one or two markets or to the specific approach of a trading technique.

Have you ever tried juggling? It's pretty hard to learn to keep three balls in the area at one time. Most people can learn to watch those 'details' after about 3 hours or practice. Add one ball, one more detail to the mess, and few, very few, people can make it as a juggler. It's precisely that difficult to keep your eyes on just one more 'chunk' of data.

Looks at the great athletes - they focus on one sport. Artists work on one primary business, musicians don't sing country western and Opera and become stars. The better your focus, in whatever you do, the greater your success will become.

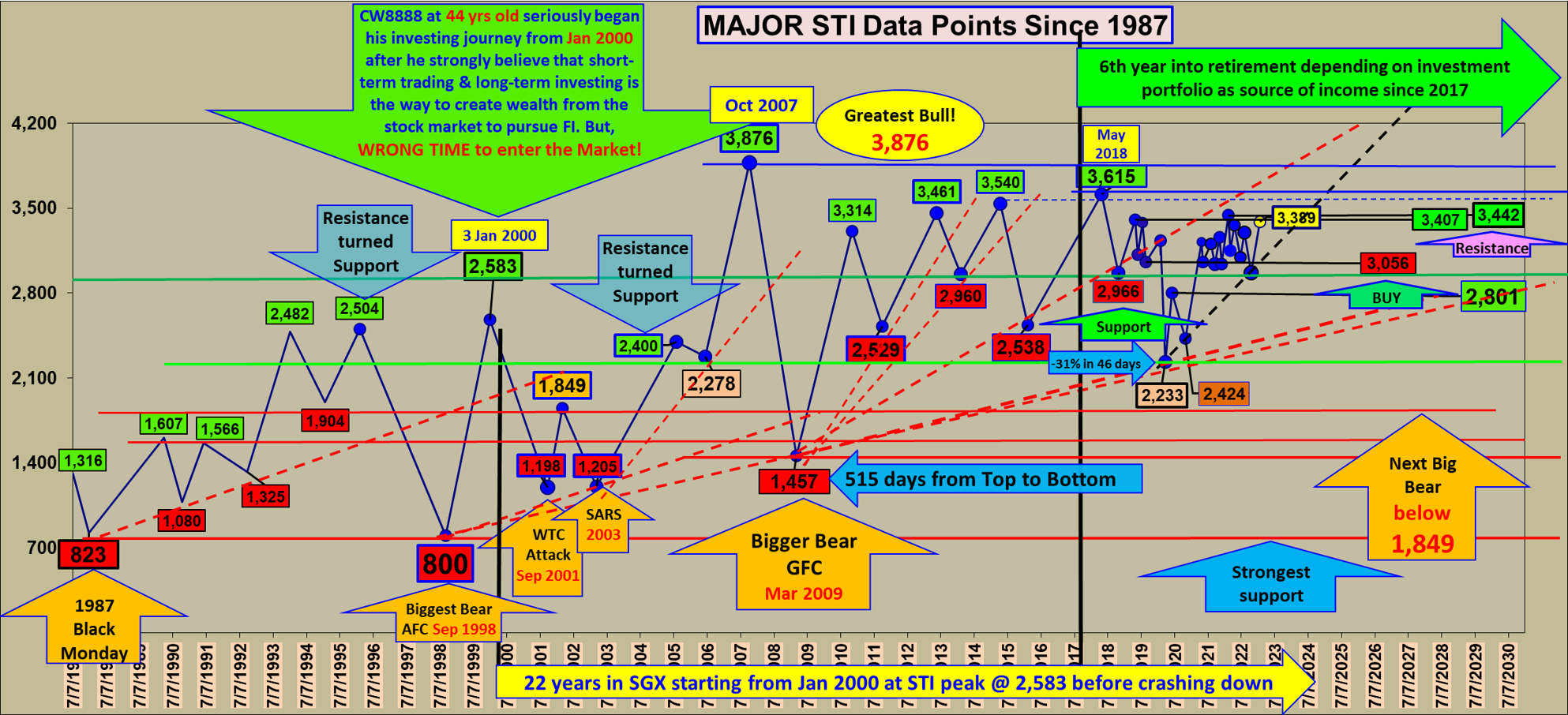

Uncle8888 re-learnt Rule 9 and testified it!

Read? Lion HST vs CSOP HS Tech (3)

First time stepping out of local market into HK Tech and kena whacked big time and never again! KNS!

The worst performing stock in Uncle8888's portfolio down -49% without a single cent of Panadol to ease heartache! Pain at the Max!

10. When in doubt, or all else fails - go back to Rule One.

So, you have money management under control, have a valid system, approach or premise to act upon - you still need control of yourself.