I started serious Investing Journey in Jan 2000 to create wealth through long-term investing and short-term trading; but as from April 2013 my Journey in Investinghas changed to create Retirement Income for Life till 85 years old in 2041 for two persons over market cycles of Bull and Bear.

Since 2017 after retiring from full-time job as employee; I am moving towards Investing Nirvana - Freehold Investment Income for Life investing strategy where 100% of investment income from portfolio investment is cashed out to support household expenses i.e. not a single cent of re-investing!

It is 57% (2017 to Aug 2022) to the Land of Investing Nirvana - Freehold Income for Life!

This blog is authored by an old multi-bagger blue chips stock picker uncle from HDB heartland!

"The market is not your mother. It consists of tough men and women who look for ways to take money away from you instead of pouring milk into your mouth."- Dr. Alexander Elder

"For the things we have to learn before we can do them, we learn by doing them." - Aristotle

It is here where I share with you how I did it! FREE Education in stock market wisdom.

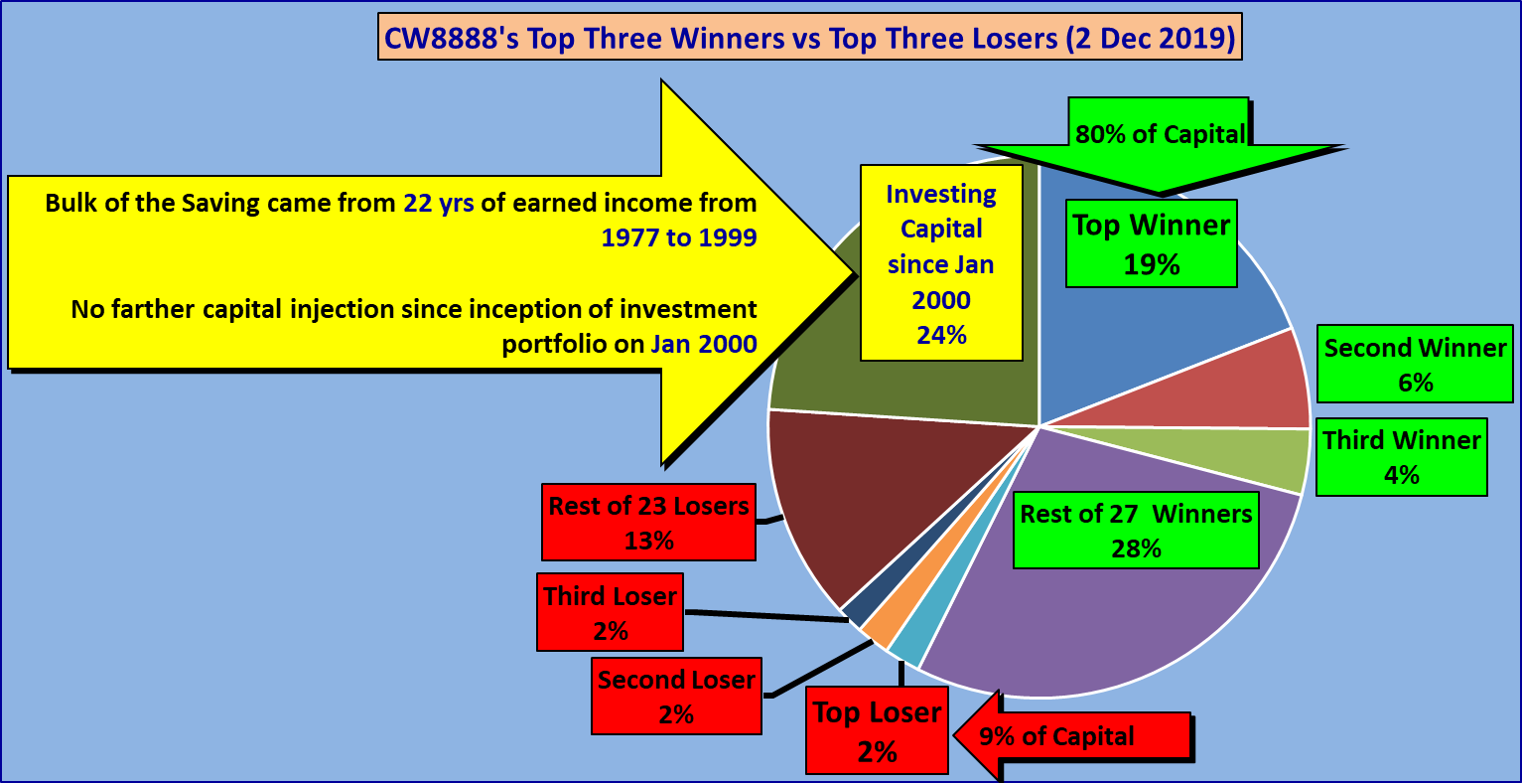

20 years of data points and back-testing Read? Peter Lynch on His Secret to Superior Returns Uncle8888's 20 years of data points by back-testing; it also provided the evidence that it is worth the time, effort, patience, and discipline to build larger war chest and systematically deploys this war chest with right position sizing over a bigger number of stocks particularly fallen blue chips during market crash. Position sizing for each counter has to be right; and the number of different counters to diversify across the market crash will depend on fire power of our war chest. Simpler to execute???

We live, earn, spend, save and invest! 20 years worth of statistics for one data point in Singapore. (1) Earned income after tax (2) Earned income after tax and excluding CPF i.e. cash available for spending (3) Household expenses for family of five; and supporting three children up to completion of their local university study (4) Net investment gains from investing stocks in SGX (5) CPF mandatory contributions Hmm ... the financial capability to inject regular investing capital into his investment portfolio is his weakness in this 20 years of investing journey. :-(

20 years across market cycles of Bulls and Bears; Uncle8888 is finding harder and harder to understand these common investing lessons/wisdom prescribed by many investment writers! 1. It’s impossible to predict the market 2. Stay focused on long-term returns It may be true for someone who has accumulated some investing capital from their savings and just begins to invest for the first time.

Don't try to predict the market and start investing!

But; for veteran retail investors who have been through one or more market cycles themselves may know that that these two lessons may not be really wise!

1. It’s impossible to predict the market

2. Stay focused on long-term returns

Yes. It is impossible to predict the market; but the next market crash will certainly and definitely happen!

Unless some Gurus can come out with a solid model to construct a defensive investment portfolio that will NOT plunge 30% to 50% from the last peak value of our investment portfolio during market crashes; then (1) and (2) are worth believing!

Hmm ... nowadays; no Gurus are conducting courses on Permanent Portfolio. How come?

After embarrassing investing method, strategies, and money management from 2006 to 2007; Uncle8888's understanding on (1) and (2) has changed.

(1) It is impossible to predict the market; but we can still choose to earn very low return and preparing large fire power to achieve Barbell return at the next market cycle!

(2) Focus on long-term returns over market cycles is NOT about taking those plunges during market crashes and then recovering back to the previous peak value of investment portfolio or higher during the next Bulls with positive returns over long-term.

We may take years to accumulate those paper gains but losing them in just one to two years; and then will take another more years just to recover back these paper losses.

Those financially stronger retail investors may recover differently and faster from these paper losses by injecting more and more capital into their investment portfolio.

Read? One Uncommon Act Of Kindness! (6) This should be a rare incident happening at LRT station! How to release someone trapped in LRT station??? Punggol Nibong LRT station which doesn't have a control room. When Uncle8888 tapped out his card to exit LRT gantry gate; he did notice the man at the adjacent gantry gate encountered error when he tapped his wallet. This is common sight happening at any MRT/LRT gantry gate. Nothing unusual about it! Uncle8888 went to location map board to locate the right staircase Exit leading to the HDB block that he was going to. But when he passed by the gantry gates again; he saw that same man who was looking stunned as he was trapped inside LRT and probably thinking how to exit since he couldn't tap out due to card error. Uncle8888 approached him and thinking how to help him. There is no control room to reset card! How? Hmm .. then Uncle8888 asked the man to come to the Entry gate and he tapped his card to open the gate and the man quickly walked out! Uncle8888 is on monthly pass so no issue of fare reduction. Okay lah! LOL! But, now Uncle8888 knew that his card would have issue to enter as the card was not tapped out. Hmm .. need to tap out!

So Uncle8888 from outside and stretched forward to tap his card on the Exit. Done! All these actions certainly were captured on LRT station CCTV. Hopefully; he doesn't get called by Police for investigation! :-( Good deed ended up with troublesome!

Read? I am on Retirement Sum Scheme (RSS) (3) So based from CPF official reply ... We refer to your enquiry of 20 December 2019. We'd like to clarify that your payout will be calculated based on your current Retirement Account savings, to last you up to 20 years from your payout eligibility age (i.e. 65), with a base interest of 4% a year. The extra interest paid by the Government (up to 2% per year) on your Retirement Account savings will be used to extend your payouts beyond 20 years, capped at your age of 90. Members who are concerned about the risk of outliving their savings can consider joining CPF LIFE before age 80. This will eliminate longevity risk as they will receive CPF LIFE payouts for as long as they live. (1) your payout will be calculated based on your current Retirement Account savings, to last you up to 20 years from your payout eligibility age (i.e. 65), with a base interest of 4% a year. Uncle8888's monthly payout from 65 to 85 is estimated to be $1,180

The extended monthly payout from 86 to 90 is calculated based on

the extra interest paid by the Government (up to 2% per year) on your Retirement Account savings will be used to extend your payouts beyond 20 years, capped at your age of 90.

After 20 years in the stock market; his own data points show clearly on the debate on Market Timer for capital gains vs Buy and Hold for dividends; who will win bigger in the Game? Market Timer will require great craftsmanship to win big; while the Time in the Market will need mental strength to stay stronger to receive stream of Panadaols to ease heartache over volatility.

How would you update your advice today? If you cannot find growth companies in innings three through five of the ballgame, look at turnarounds, special situations, back at the cyclicals. There’s a real shortage now of growth companies. That is a red flag, because all the money is flowing into [a few companies]. There’s an end to that game. It will scare me if this trend continues for a couple more years. What’s your view of unicorns? That’s a big difference today—companies stay private a lot longer. The next Google might stay private for an extra 10 years. That makes it more difficult [for individual investors]. The day they come public, a thousand organizations have looked at it, and they’re probably pretty fairly priced. Fidelity can put 5% of funds into these things. The public can’t do that. I’d rather look at something that’s been around for a long time. Where are the opportunities now? I’m looking at industries that are doing badly; that for some reason will get better. Shipping. If you want to buy a ship, it’s a two- or three-year wait. People haven’t ordered ships for a long time, because by the time one comes in, prices may be down again.

Energy services is awful; that could have a major turn in the next year or two. Oil is interesting. Look, longer term, solar, windmills really work. But you need natural gas and oil to bridge to this. Everybody’s assuming the world’s going to not use oil for the next 20 years, or next year. China might sell five million electric vehicles next year, but they might also sell 17 million internal combustion engines. They don’t have old cars to retire. There are no electric airplanes. Near term, liquid natural gas and liquid petroleum gas might replace diesel fuel for trucks. I’m buying companies that I don’t think will go bankrupt. They’ve got to be around the next 18 to 24 months, or I have no interest. Anything else do you want investors to know?

If you’re going to invest, you have to follow certain rules. If you want to ski, you ought to go to the bunny hill and learn how to stop. It doesn’t make you an Olympic skier, but then in certain cases, you have an edge on the Fidelitys of the world. You might be in the cement industry, and suddenly orders pick up. You can see things better. The one thing I want everybody who is buying individual stocks to get is that they have to understand the story, the five reasons something is going to go right for the company. If you can’t convince an 8-year-old why you own this thing, you probably shouldn’t own it. Don’t invest in a company before you look at the financials. If you made it through fifth grade, you can handle the math.

Read? Dec 2019 Investing Performance Report : 20 Years in local SGX stock market only The moral story of Grasshopper and Ant in the stock market From 2000 to 2007; Uncle8888 was the Grasshopper in the stock market and especially from 2006 to 2007 singing loudly and cheeerfully in the Summer Bull. Bom pi pi! Setting new record high one after another without injecting a single cent as capital into his investment portfolio. In the Summer; why Grasshopper wants to worry about Winter like Ant. Waste time and waste opportunity to enjoy the Boom! Then what happened after next? 8 years of slow climb to the Peak in the Summer 2007 and just one yearto rapid fall to the Low in the Winter 2009! Then it took another 9 long years just to recover from the last Winter and set a new record high in Jan 2018! 10 long years of Summer! Ant has accumulated so much food to survive the Winter and the food is rotting in the Freezer! A long, long boring Summer for the Ant! What next for the Ant? Read? My Own Psychology Of Losses: Losing Money And Deploying Cash Is Not The Same!

Based on Uncle8888 DIY calculator on his computed RA balance at 65. The CPF estimated monthly payout of $1,180 for 23 years estimated duration is close to his own calculation based on 4% CPF RA compound interest. However; what is the monthly payout after 23 years from those accumulated extra interests compounded over 35 years is NOT known? CPF calculator stopped functioning!!! Spoil liao!!! LOL! Retirement Sum Scheme QWhy is extra interest used to extend payout duration by up to 5 years after age 85 and not use extra interest to increase payout amount? A

Using extra interest to extend payout duration ensures that more members are protected against the risk of outliving their payouts. In 2018, more than half of residents aged 65 were expected to live beyond age 85. This would mean that the majority of members on Retirement Sum Scheme (RSS) would outlive their payouts if the extra interest is not used to extend payouts for up to five years. With the extension of RSS payouts up to age 90, up to two in three members will have protection against the risk of outlving their payouts.

Three years have passed ... Replacement income for the last three years since 2017

Monthly and annual household expenses

Projected impact of year-on-year inflation on household expenses didn't seen to happen. Somehow we will react to some price increase and make adjustment for alternatives. Yearly Cash-In and Cash-Out Spending below replacement income and manage to have some small savings over the last three years.

So far, Uncle8888 has received five good/kind intention of advice/suggestions to get a proper job with CPF and medical benefits. Two out of the five advice/suggestions is to go for fully subsidized course to get certification since Uncle8888 is still eligible for these subsidies. As response to their advice/suggestion Uncle8888 showed them ..

The moral of story ... Don't anyhow suggest/give advice without knowing someone more in depth; and especially true for investment blogger like Uncle8888!

If you're looking for an eco-friendly vacation spot where you can enjoy the beautiful scenery while walking on a well-maintained trail to stay fit, there's no better place to go than Jeju Island. In the local dialect, "olle" originally referred to the narrow path between the street and one's doorstep. Jeju Olle-gil, a series of walking trails that stretchs around the entire coast of the island, is one of the many attractions and activities that Jeju has to offer. The trails pass through various landscapes along the way, including small villages, beaches, farms and forests. Each route offers a unique opportunity to soak in the beauty of Jeju and the island's culture. There is currently a total of 26 routes, consisting of 21 main routes and five sub-routes. Each course differs in length and difficulty, allowing visitors to choose the appropriate course that meets each individual’s level. The shortest route takes approximately one hour and the longest up to eight hours to complete. As each course is equipped with directions and guiding posts along the way, even first-time visitors will be able follow the trail conveniently. Visitors can get more information about Jeju Olle-gil Trail by visiting the official website.

Uncle8888 plans to walk Route 1, 6, 7 and 18; and if still have time will do Route 10 too.

4 Hallasan Trails – Which one is best and how to get there? There are four Hallasan trails on and around the mountain, but only two of these trails will take you all the way up to the volcano’s crater lip – the Gwaneumsa trail, and the Seongpanak trail: Gwaneumsa Trail – 8.7km (one-way) and 8-10 hours return hike <– the BEST views! Seongpanak Trail – 9.6km (one-way) and 7-9 hours return hike <– the EASIEST hike! Eorimok Trail – 4.7km (one-way) and 2.5 hours return hike

Yeongsil Trail – 3.7km (one-way) and 2 hours return

After the last trip of steep walking up to Aowanda (奧萬大) suspension bridge; Auntie8888 is quite weary of another steep walking up mountain hike. LOL! So forget about best view!

No need for Opposition party to form the next Govt to return my CPF. Just a few clicks on 'my cpf Online Services' and demand PayNow! Few seconds later, Uncle8888 received his CPF payment!

Thank you for using 'my cpf Online Services'.

We refer to your withdrawal application for members age 55 and above - Payment via PayNow (Transaction Number) submitted on 05 Dec 2019. Your application has been successfully processed. The payment has been credited to your bank account linked to your Singapore NRIC under PayNow. $24K CPF Interests Withdrawal 1) Deducted interests from SA first i.e. Jan to Nov (11 months) is $1,534.94 2) Remaining balance deducted from OA i.e. $22,465.06

Read something interesting : The Fund’s Performance is not Your Performance Hmm ... then similarly it is also true for .. The Trainer's/Blogger's/ETC's Performance is not Your Performance. Tio bo?

Uncle8888 was surprised when the dental counter staff said no payment is required. FREE? Arh! Hmm! When he looked at the bill ... OIC! Lucky Merdeka generation after Pioneer generation who has better subsidies from Big Daddy!

Uncle8888 enjoyed his first Merdeka Generation Benefit #3 Outpatient Care Subsidies - Additional 25% off remaining bill for subsidised services and medications.

Read? More on Pareto blog posts The secret to winning in the Pareto principle in investing is .... position sizing and size of war chest during market crashes! Updated on 2 Dec 2019

Long term investing is all about recognizing market cycles exist and then figure out for ourselves how much money from the stock market we can comfortably received and keep it safely from giving back at the next Bear.

Patience, discipline and financial capacity to accept this trade off and expecting larger and better outcome when that opportunity finally strikes!

Get real and don't be fooled by illusion of wealth in bullish stock market! Read? My Own Psychology Of Losses: Losing Money And Deploying Cash Is Not The Same! 20 years in the stock market; probably Uncle8888 had seen what is real and what is just an illusion! STI, Stock Value and War Chest across past market cycles

STI, Stock Value, War Chest and Cash Flow across past market cycles

Read? Discovering Johore by Bus and Walk - Mersing Monday, 23 March 2015 Kota Tinggi - Larkin RM 4.80. Friday, 29 Nov 2019 After 4 yrs, still RM 4.80 But, with minor trade off. Bus still has air - "con" and good life span!

SINGAPORE - People in the Republic are contributing more to their retirement funds, said the Central Provident Fund Board in a statement on Thursday (Nov 28). Singaporeans added nearly $1.6 billion in total under the Retirement Sum Topping-Up Scheme between January and October. CW8888: Wow! Of course, we love our CPF Retirement scheme! Please keep our money with CPF to compound at 4%. Bom pi pi! Hmm ... Those opposition parties campaigning on Return My CPF to form the next government still got chance ah??? CPF lovers over-run CPF haters! No?

The total top-up amount was an increase from $1.5 billion over the same period last year. CPF members topped up a total of $2 billion to their accounts for the whole of 2018. In 2015, the total top-up amount was $934 million. The scheme helps people to build their retirement savings by topping up their own Special Account or Retirement Account, or those of their loved ones. "These top-ups, which comprise cash top-ups and CPF transfers, help build up members' retirement savings. With higher CPF bala nces, these members would receive higher payouts in their retirement years," the CPF Board said. Members have also been able to have the Basic Retirement Sum, or more, in their CPF accounts as a result of the top-ups received, said the board. Over the last three years, close to 24,000 members attained the Basic Retirement Sum, or more, after receiving top-ups to their CPF.

SINGAPORE: Workers in Singapore received a bump of 2.2 per cent in their income in 2019, according to the Labour Force in Singapore Advance Release report released on Thursday (Nov 28).

The nominal median income of Singapore residents on full-time employment increased this year toS$4,563from the S$4,437 recorded in 2018, the Ministry of Manpower (MOM) report said.

This year's 2.2 per cent real income growth is lower than the growth of 4.4 per cent in 2018.

From 2014 to 2019, real median income increased by 3.8 per cent annually - "significantly higher" than the 1.9 per cent annual growth in the preceding five years.

The findings were based on the Comprehensive Labour Force Survey conducted in mid-2019 by the ministry's research and statistics department.

Low-wage workers - those at the 20th percentile - experienced 4.4 per cent annual growth in median income from 2014 to 2019, higher than the 3.8 per cent growth for those at the 50th percentile and significantly higher than in the preceding five years.

Unemployment rate of resident PMETs and non-PMETs. (Graphics: MOM)

UNEMPLOYMENT RATE FOR NON-PMETS RISES

Unemployment among non-PMETs increased to 4.7 in June 2019 from 4.0 per cent a year prior, due to cyclical effects such as the US-China trade conflict which affected manufacturing output and retail trade.

But the increase in their long-term unemployment rate was "slight" - from 0.7 per cent to 0.8 per cent.

The proportion of resident workers on fixed-term contracts continued to increase to 7.6 per cent from 7.2 per cent last year, indicating that employers are more cautious on hiring amid uncertainty.

Permanent employees continued to form the vast majority among resident employees, even though their share dipped slightly from from 89.4 per cent to 89.3 per cent.

The ministry said it is closely monitoring the labour market with Workforce Singapore, and will support Singaporeans' employment through the Adapt and Grow initiative.

"We also encourage jobseekers to be open to opportunities in other sectors and occupations beyond what they are familiar with," it added.

Commenting on the labour report, Manpower Minister Josephine Teo said that the current outlook can be described as "persistent showers but with pockets of sunshine".

Mrs Teo said that in spite of economic headwinds, companies were still hiring and local employment continued to grow.

Even in sectors hit by the trade tensions like manufacturing, there were about 6,000 manufacturing job vacancies in June this year.

"That will remain our focus: Help people enter into jobs where there is potential for growth, where there's potential for advancement," she said.

Source: CNA/jt(rw) Read more at https://www.channelnewsasia.com/news/singapore/singapore-income-wages-labour-market-report-mom-12133236

60% of Singaporeans Live Paycheck to Paycheck

-

A recently published report from global payroll and HR solutions provider

ADP featured in a Singapore Business Review article reveals a staggering

truth ...

Top 10 Highlights of 2024

-

As a dragon baby navigating the Year of the Dragon, it is inevitable that I

experienced more downs than ups in 2024. Whether it is at work, familial

rela...

Rolf 2023 in Review, Looking forward to 2024!

-

Happy new year to all. This post came late. But better late than never,

:-). Looking back, 2023 has been one of the most eventful

The post Rolf 2023 in R...

Hello SP Group, I'm Back!

-

Yup, I've moved back to Big Daddy's electricity provider this month.

To recap and have a better sense of context, you may want to read my

previous 18...

Farewell, Uncle CW8888

-

On 8 April 2023, I lost a friend.

To honour the memory of Uncle CW8888, let me share a few nuggets of wisdom

I have learned from him as well as some of t...

To my beloved friend CW8888

-

It is with infinite sadness that I came out from my hiding hole to blog

about the passing of a dear friend, CW8888, whom I affectionately call

senior bro...

Festina Lente Redux - Five years down the road

-

A big apology to the few readers (if any) who read this blog.

About five years so, I had made a pivot to ETF based exposure to a global

financial portfo...

January 2020 - Yaruzi's Portfolio Update

-

I received a sad news from a close family friend in January, two weeks

before Chinese New Year. Our dear friends lost their beloved and only son

due to sic...

Happy new year 2020 and review of 2019

-

Happy new year 2020! Wow! So fast! Another year has passed by..

Year

My Portfolio

(inclusive of capital injections)

My Portfolio (less capital injections)

S...

Being Frugal or Being Cheapskate?

-

Everyone is born with a different spoon in their mouth. Some entered the

world with a golden spoon right up while some are out with a plastic one.

Nonethel...

Get big Muscles with Testosteron improvement

-

Muskelaufbautraining mit Nahrungsergänzungen wie macht man das richtig?

Muskelaufbau ist nicht einfach und schnell, wie es viele Sportler erwarten

geht ...

Frasers Logistics and Industrial Trust

-

Another REIT is going IPO, this times, it's an Australian pure-play REIT

with logistics and industrial properties, Frasers Logistics and Industrial

Trust. ...

-

*Welcome to Singapore Investment Bloggers!*

This site provides an updated listing of investment blogs based in

Singapore.

If you would like your blog t...

Last updated : 24 Sep 2022

I am 66 yrs old uncle living in HDB heartland who has achieved financial independence @ 56 and finally retired @ 60 from full-time job as employee on 1 Oct 2016.

Single household income since 1995 with three children.

Currently, two sons and one daughter are working.

I have been doing 22 years of long-term investing and short-term trading in Singapore stock market only since Jan 2000 so I am that so-called Panda or Koala in the investment world.

Currently, I am on my way to Investing Nirvana - Freehold Investment Income for Life after 23 years of building up Investment Portfolio through long-term investing for growth-dividends and short-term trading on Rounds after Rounds.

I have also achieved sustainable retirement income for life from CPF and Year-on-year Diminishing Bear Market Impact stock Investment Portfolio in local market, SGX! i.e. Beary Safe!

Cheers!

Disclaimer: Stock trading involves significant risks. Create Wealth trader is not a licensed Investment Adviser and will not be responsible for any losses which you incurred. You are advised to always do your own homework before making any trading decision.