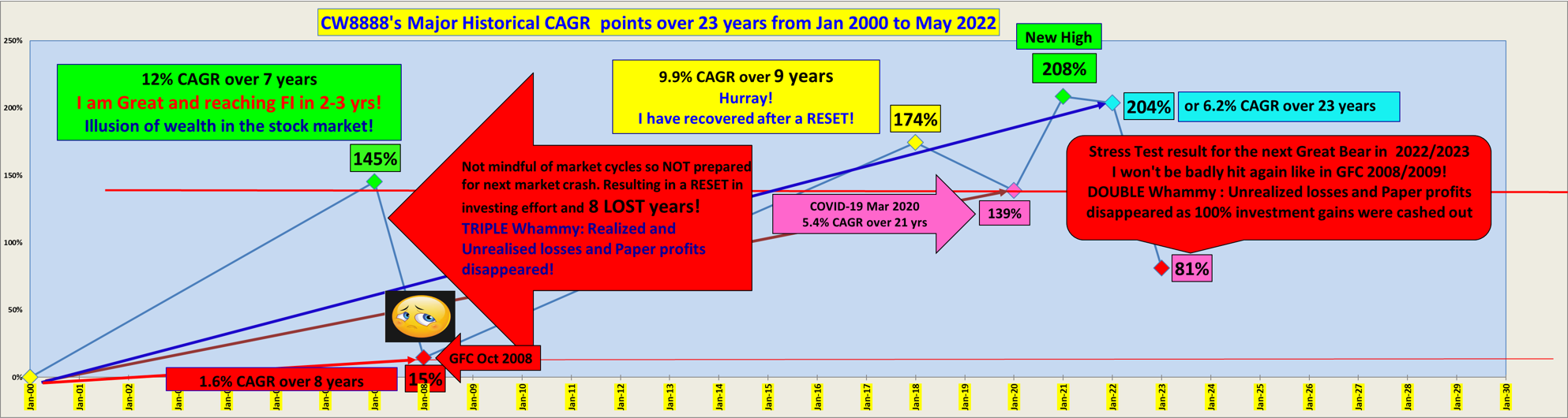

This is how Uncle8888 as retiree has reduced from Triple Whammy in the last GFC Bear in 2008/2009 to Double Whammy in the next Bear market!

Triple Whammy: Realized losses, Unrealized losses and Paper profits disappeared fast!

Double Whammy : Just Unrealized losses and Paper profits disappeared fast as 100% of realized profits and dividends will be cashed out to Cash Reservoir to support future household expenses.

Using only invested capital recycling strategy in the investment portfolio to generate retirement income for life!

Recovered invested capital not yet recycled into the market is in the war chest. Not bluffing. Technically right. LoL!

ReplyDeleteCW,

ReplyDeleteI hope I have the wisdom the walk out of the casino one day...

Those who won at the casinos before know its not how much we've won, but how much we bring OUT that matters ;)

You think why casinos give free food and drinks to entice gamblers to keep on playing?

Same reason why we have brokers offering "free" trading without commissions ;)

Uncle8888,

ReplyDeleteWithout big expenses of dependents or fear of job loss, it gets a bit easier to go thru bear markets. ;)

Over the past 5 yrs, with your overall liquid networth spread mainly over CPF, stocks & a 2-year household expenses current account, I believe you've constructed a self-sustaining system to handle the 3 things for retirees:

1. Daily living expenses (including occasional repairs & replacements of fridge, washing machine, aircon etc)

2. Medical (big hits or long term expenses)

3. Leisure & extra luxuries.

Going back to your previous posts about position sizing...

One can rest easy even with a major hit to a 10% stock position when that comes from a stock portfolio that is 1/3 the amount of the CPF portion. ;)

However it does mean ensuring S'pore remains a growth story, with:

1. Strong SAF

2. Open city & open policies

3. Be willing to discard old industries & old ideas, creative destruction even if it means large unemployment for locals temporarily.

I hope the third point unemployment for local temporary would not become a trend and permanent yeah .

DeleteThanks for sharing CW.

ReplyDeleteI have many retired friends & colleagues in the 60s to 70 age group, but none willing to share details on their cashflow and expenses and whether things are panning out according to their plans.

What I observed in general was that those who retired in their 50s tended to have cut back on their lifestyle (most still own cars) while those that retired later (in their 60s) seemed to be maintaining the same lifestyle as when they were working, ie still buying new cars and travelling. Maybe those that retired earlier (in their 50s) have done their share of travelling upon retirement and now living the simpler lifestyle.

None has downgraded from their dwelling, while one actually upgraded from HDB to a condo. Among the late retirees, two stood out. They both own 2nd properties and didnt bother to rent them out for rental income!

After witnessing that our dividend income tap was not reliable nor stable, we are not sure if I should still continue to invest for dividend income as I approach retirement. Our original goal was to aim for an average monthly income $6,000 from this dividend tap but now that conviction has wavered. Our dividend income has averaged slightly above $5,000 per month over the last three years. We have since relegated the dividend income tap and the rental tap to "bonus taps" meaning we will not be depending on them to sustain our retirement. If got dividend and rental incomes, they will be bonus for us to pamper ourselves.

Our main sources of income will then be interests from our OA & SA, SRS drawdown, and CPF Life payout. Together they could bring us about $10K per month and our retirement lifestyle will be based on that.

Yeap. We cannot just depend on dividends as it is rather unstable over economic cycles. CPF can be our stable fixed income in addition to dividends. That why 1M65 is attractive to younger generation. Start saving more!

DeleteCPF change rules cannot withdraw interest

DeleteYa. That why I transferred SA to RA to live with the changed rule. What will be the next shifting goal post?

Delete